ThinkOrSwim Backtesters

Test your trading strategies on historical data before risking real money. Download free thinkScript backtesters or learn to build your own from scratch.

Popular ThinkOrSwim Backtesters

These are our most-used backtesters for validating trading strategies in ThinkOrSwim.

Build an Election Backtester in 10 Minutes

Backtest how often the markets rally after each U.S. election, to find common patterns post 30 days, 60 days, and 90 days.

Download Free → Free

Free

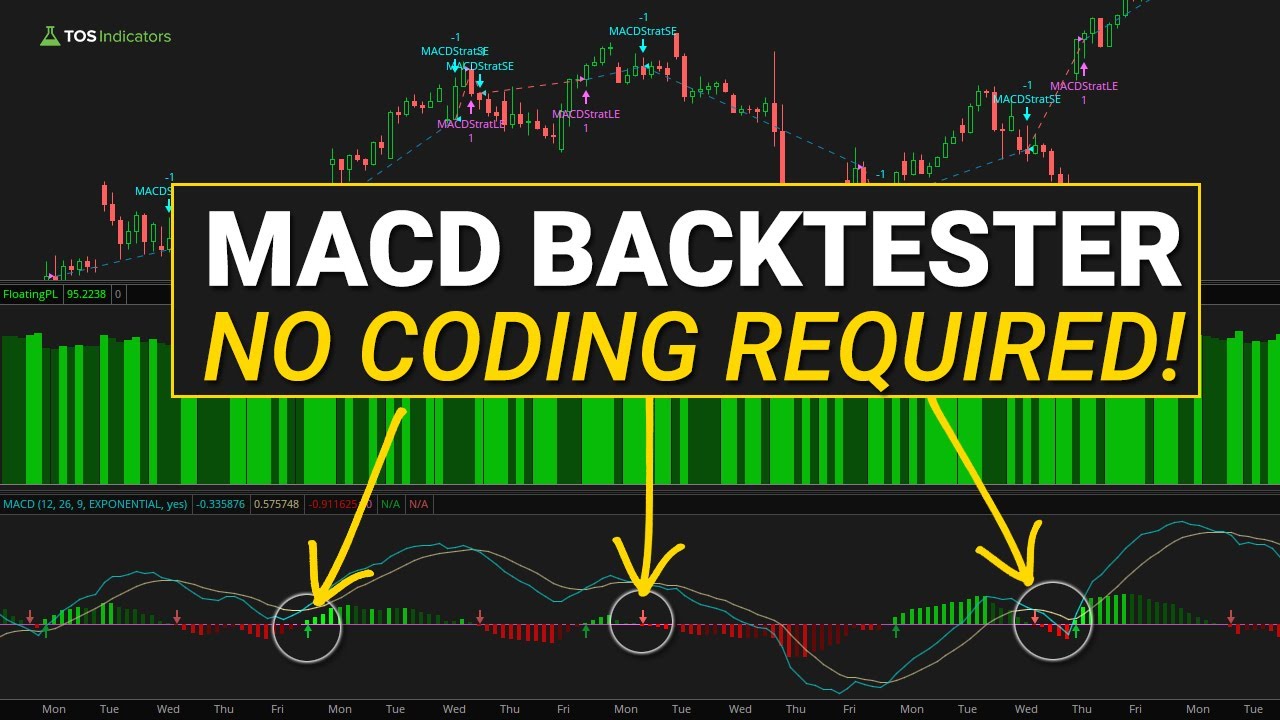

Moving Average Crossover Backtester

Learn to build two advanced ATR scans in ThinkOrSwim. Discover stocks with high volatility and compression patterns near key moving averages.

Download Free →

Moving Average Pullback Backtester

Test whether moving average pullbacks are effective, and if so, which moving average is best for your favorite markets.

Download Free →

Opening Range Breakout

Master dynamic opening range breakouts with customizable time frames and smart alerts. Track projection levels, pullbacks, and validate strategies with integrated backtesting capabilities.

Learn More →

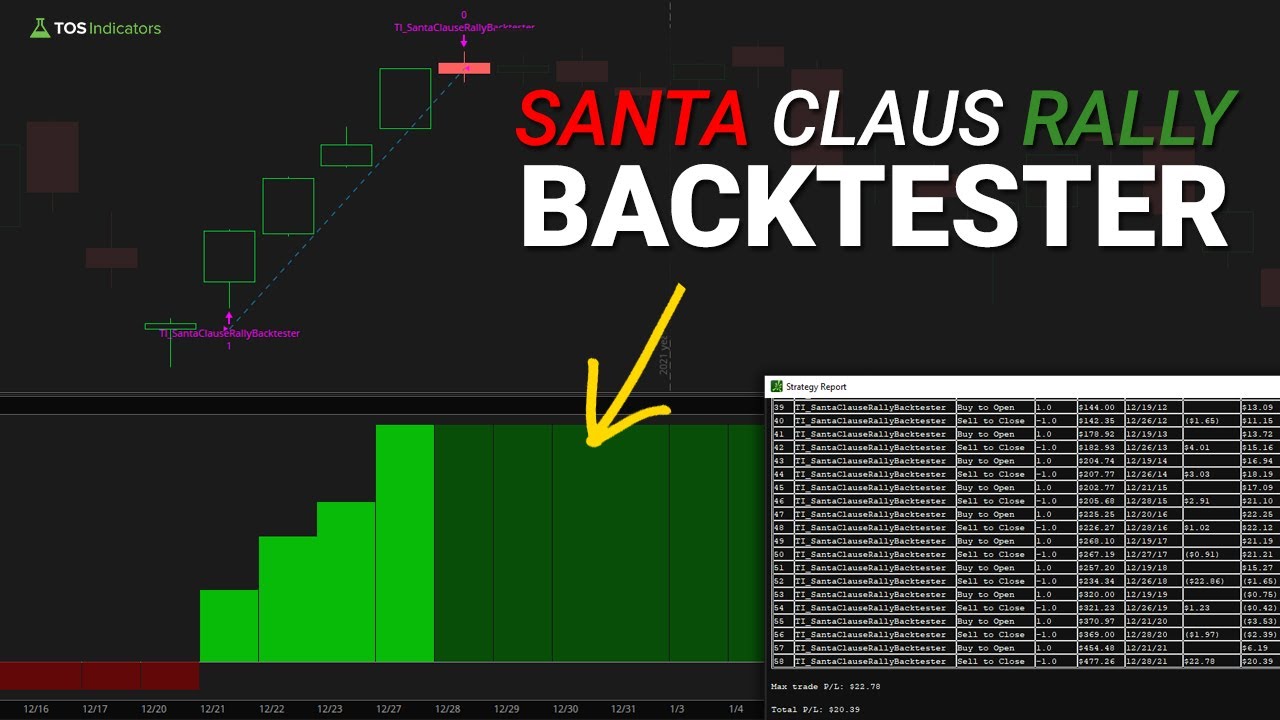

Santa Claus Rally Backtester

Learn to build two powerful ATR scans in ThinkOrSwim: Identify high-volatility stocks and find consolidations near key moving averages. Boost trading decisions with volatility-based filtering and trend alignment.

Download Free →

SPY Meltdown Backtester

Test what happens the day after a meltdown in the S&P 500 - do we see continued selling, or do buyers stage a short term rally?

Download Free →All ThinkOrSwim Backtesters

Browse our complete library of thinkScript backtesters with code and tutorials.

Backtesters 8 backtesters

Build an Election Backtester in 10 Minutes

Backtest how often the markets rally after each U.S. election, to find common patterns post 30 days, 60 days, and 90 days.

Moving Average Crossover Backtester

Learn to build two advanced ATR scans in ThinkOrSwim. Discover stocks with high volatility and compression patterns near key moving averages.

Moving Average Pullback Backtester

Test whether moving average pullbacks are effective, and if so, which moving average is best for your favorite markets.

Opening Range Breakout Pro

Master dynamic opening range breakouts with customizable time frames and smart alerts. Track projection levels, pullbacks, and validate strategies with integrated backtesting capabilities.

Santa Claus Rally Backtester

Learn to build two powerful ATR scans in ThinkOrSwim: Identify high-volatility stocks and find consolidations near key moving averages. Boost trading decisions with volatility-based filtering and trend alignment.

SPY Meltdown Backtester

Test what happens the day after a meltdown in the S&P 500 - do we see continued selling, or do buyers stage a short term rally?

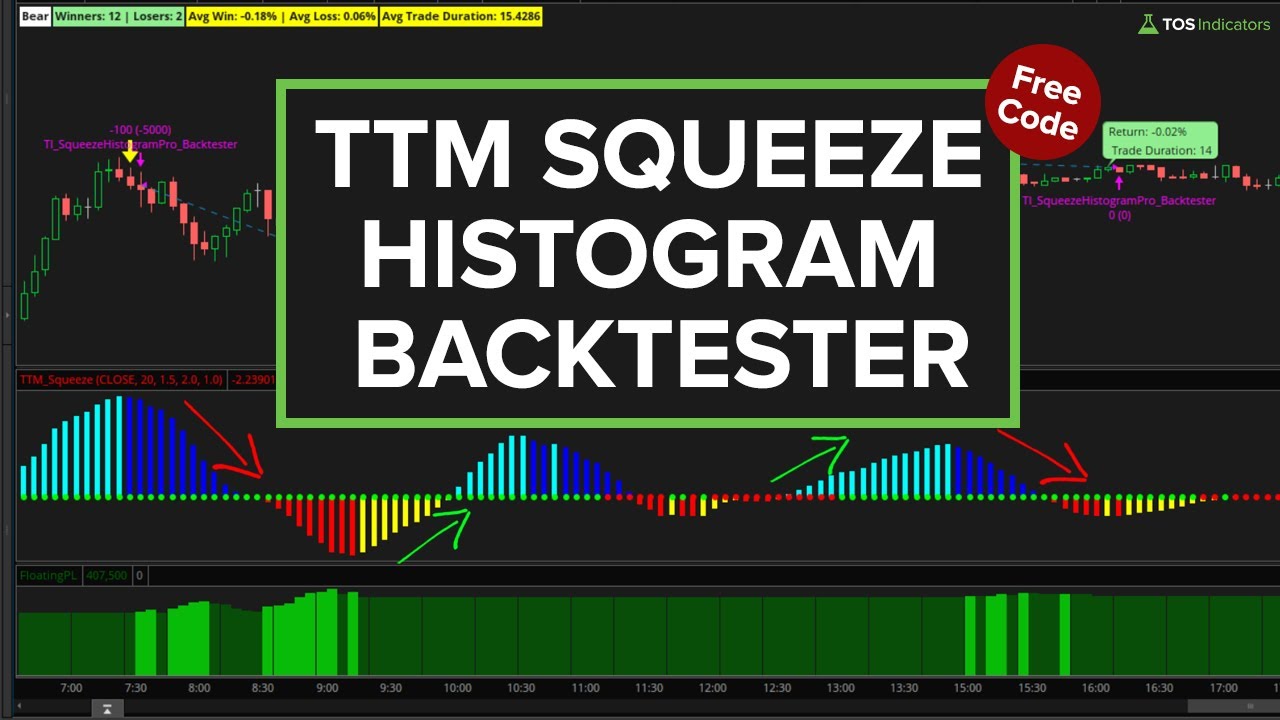

TTM Squeeze Histogram Backtester

Test if the TTM Squeeze Histogram is effective in timing momentum shifts in your favorite markets, on any time frame chart.

TTM_Squeeze – Backtest Like a Pro

Build a TTM Squeeze Backtester that allows you to test squeezes on different time frames, with to find the best nK and nBB factor settings

Squeeze Course Backtesters 4 backtesters

Triple Squeeze Backtester Course

Backtest Triple Pro Squeeze setups with customizable entry and exit rules.

Slingshot Squeeze Backtester Course

Test slingshot squeeze patterns with historical performance stats.

Squeeze Signals Backtester Course

Backtest squeeze signal entries with win rate and profit metrics.

Squeeze Histogram Backtester Course

Test momentum histogram crossover strategies on any symbol.

How to Build ThinkOrSwim Backtesters

Learn how to build your own backtesters from scratch using thinkScript with these step-by-step tutorials.

ThinkOrSwim Backtesting FAQ

Backtesting is the process of testing a trading strategy on historical data to see how it would have performed. It helps you validate ideas before risking real money, identify optimal parameters, and understand the historical win rate and risk/reward of a strategy.

Yes, ThinkOrSwim has built-in backtesting capabilities through thinkScript strategies. You can create custom strategies that generate buy/sell signals and view performance reports showing profit/loss, win rate, and trade history on any chart.

To create a backtester, write a thinkScript strategy with AddOrder() commands that define your entry and exit rules. Apply it to a chart and ThinkOrSwim will show you historical trades. Our tutorials walk you through building backtesters step-by-step.

Key metrics include win rate (percentage of profitable trades), profit factor (gross profit / gross loss), maximum drawdown, average win vs average loss, and total number of trades. A good strategy has a positive expectancy when combining win rate with reward/risk ratio.

Test across multiple market conditions including bull markets, bear markets, and sideways periods. For swing trading, 5-10 years of data is ideal. For day trading, 1-2 years may suffice. More data gives more confidence, but markets do change over time.

Avoid curve fitting (over-optimizing for past data), ignoring transaction costs, testing on too little data, and look-ahead bias (using future data in calculations). Always validate results on out-of-sample data before trading live.

ThinkOrSwim backtesting is primarily designed for stock and futures strategies. For options, you can use the thinkBack feature to view historical options chains, but automated options strategy backtesting requires external tools or manual analysis.

Look beyond just total profit. A strategy with 40% win rate can be profitable if winners are much larger than losers. Check consistency across different time periods. Be skeptical of results that seem too good to be true, as they may indicate overfitting.

Get Pro ThinkOrSwim Backtesters

Unlock advanced backtesters and course-exclusive tools with the Squeeze Course.